Estimating the cost of a product is referred as product costing. Now in order to estimate cost of any product, below information is needed

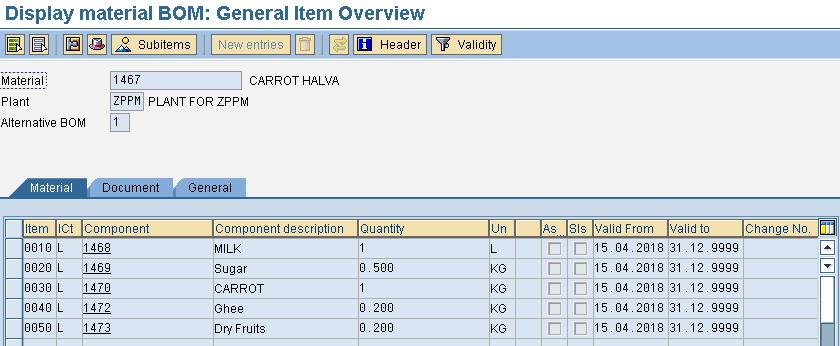

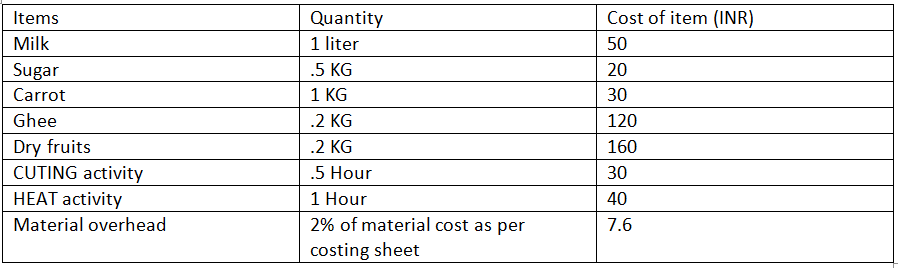

- What materials and in how much quantity are consumed in producing finished good? List of all the materials which are consumed is referred as Bill of Materials (BOM).

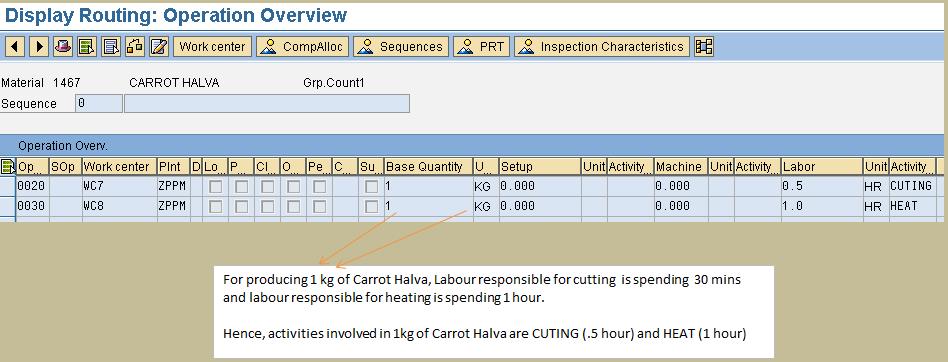

- How much is the making cost in producing finished product? Making cost comes from activities that are being performed on materials to produce finished product. Each and every activity which is performed has cost associated with it. Hence if we calculate cost of each activity and add it up, we will arrive at making cost of finished product.

Each activity might have different cost associated with it. Hence making cost of finished product depends upon which activity is performed in how much quantity in producing finished product. Hence, adding up the cost of various activities in order to arrive at making cost of finished product is referred as Activity Based Costing.

Maintaining the list of all the activities and their respective quantities which are performed in producing finished product is referred as Routing.

How much is the overhead cost in producing finished product. Overhead cost is the indirect

cost which is involved in producing finished product. Example of overhead cost Electricity, Wifi, cleaning cost, telephone bills etc.

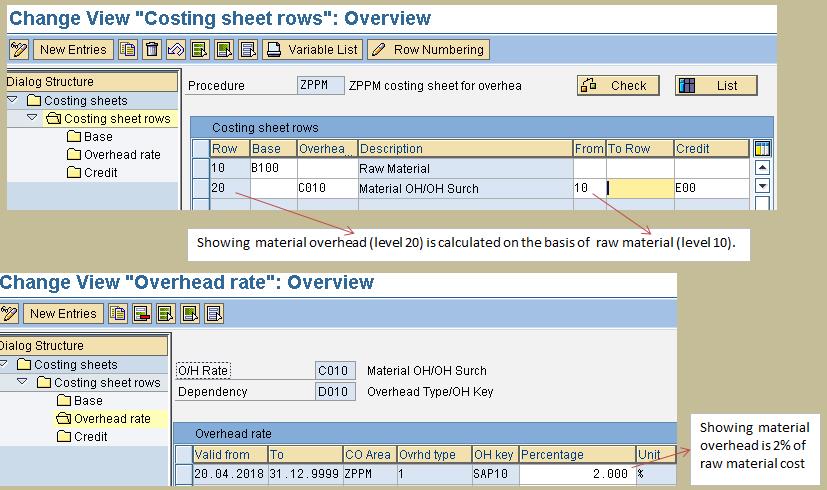

Let’s say that over the years of experience, business has learned that overhead cost is normally 1% of material cost and .5% of making cost. Hence overhead cost is calculated by applying certain % on material cost and similarly on making cost.

Hence for calculating overhead cost, we can use a formula which will calculate overhead by applying certain % on material cost and certain % on making cost. This kind of formula is referred as Costing Sheet.

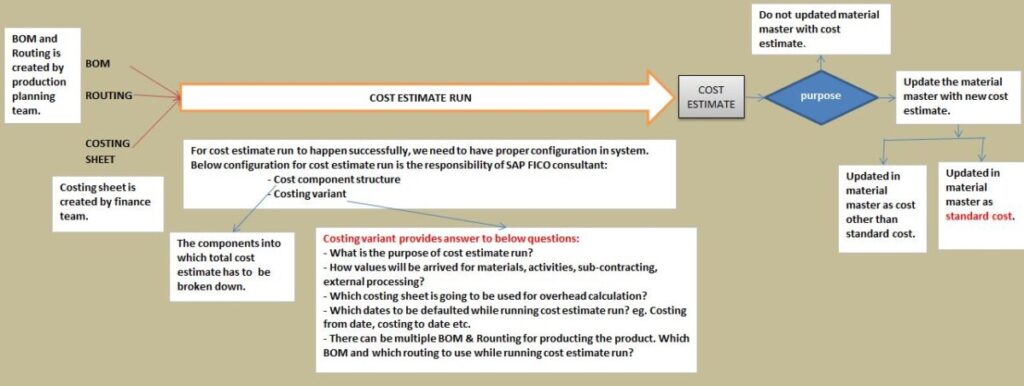

Hence to estimate cost of a finished product, we need to create BOM, Routing and Costing sheet.

Material is created by SAP MM team.

BOM and Routing is created by SAP PP team

Costing sheet is created by finance team.

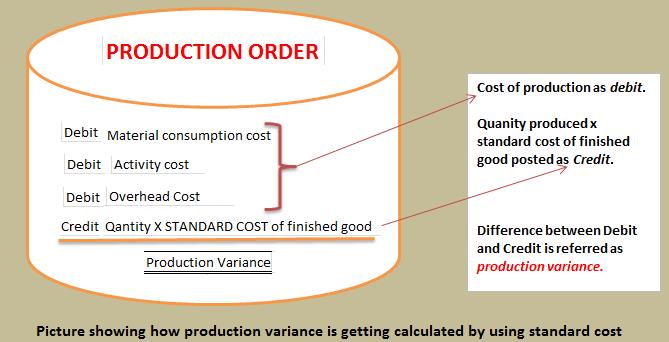

Let’s say Bom, Routing & Costing sheet is created. Then in order to estimate the cost of finished product, we need to execute cost estimate run. The estimate run picks up the list of materials consumed from BOM, picks up the list of activities from Routing and calculates overhead cost using Costing sheet.

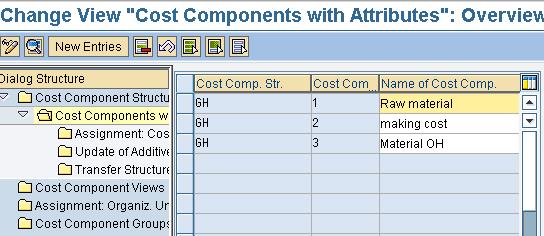

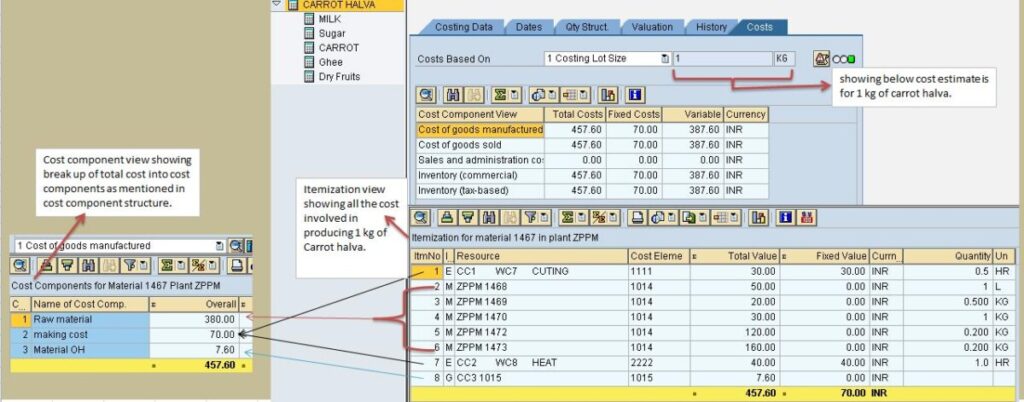

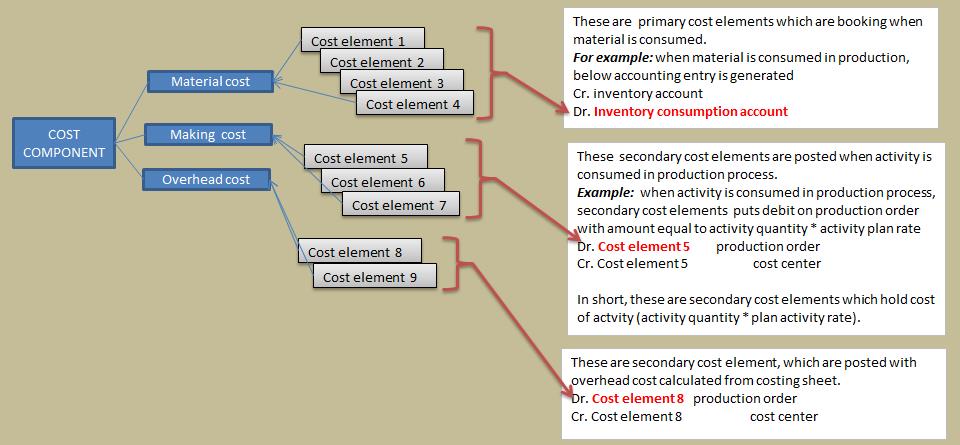

Output of cost estimate run is, estimate cost of finished product divided at lower level. Total cost of finished product is broken down at lower level for analysis purpose. These broken down lower level of Cost is referred as Cost Component.

In our example, total cost can be broken down into lower levels (cost components) like Material cost, Making cost & overhead cost. These cost components add up to make cost of finished product.