Let's first understand what is retained earnings account.

Let’s first understand what is retained earning account

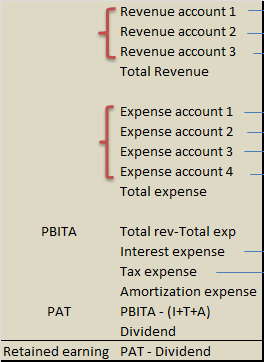

Company prepares its profit & loss statement by taking into account all the revenues and expenses.

Consider below example, company is operating since 5 years.

Opening retained earning= beginning retained earnings + net income – dividend

The current year’s retained earnings amount from profit & loss statement is taken to next year’s balance sheet on the liability side.

Now you understand the concept of retained earnings, so the next question is how is retained earnings handled in sap.

How retained earnings are handled in sap?

A GL master for retained earnings is created and declared as retained earnings account using T code: OB53.

Since retained earnings is part of shareholder’s equity which comes under balance sheet. Hence GL master of retained earnings account is created with account type ‘balance sheet’.

This retained earnings account is assigned to each and every profit & loss account.

[As per standard practice single retained earnings account is used in a company code. In such cases, once a retained earning account is declared in OB53 then sap by default assigns this retained earnings account to each and every profit & loss GL account.

But in rare cases when more than one retained earnings account is created and declared in OB53, then while creating GL master for profit & lose account one has to choose retained earnings account manually.]

At the end of year, balance carry forward program (FAGLGVTR) is executed to move balances to the next year.

Year-end balance of profit & loss account

Balance in profit & loss accounts is carried to next year using retained earnings (RE) account.

Balance amount is carried forward in local currency.

Retained earning amount is carried forward without any account assignment like cost center, profit center, internal order or WBS.

Year-end balance of balance sheet account

Year-end balance of balance sheet accounts, customer, and vendor is carried forward using the same GL account.

Balance sheet balance is carried forward with account assignment.

Note: No accounting document is posted when year end carry forward program is execucted. Balances are simply moved to next year without any document getting posted.

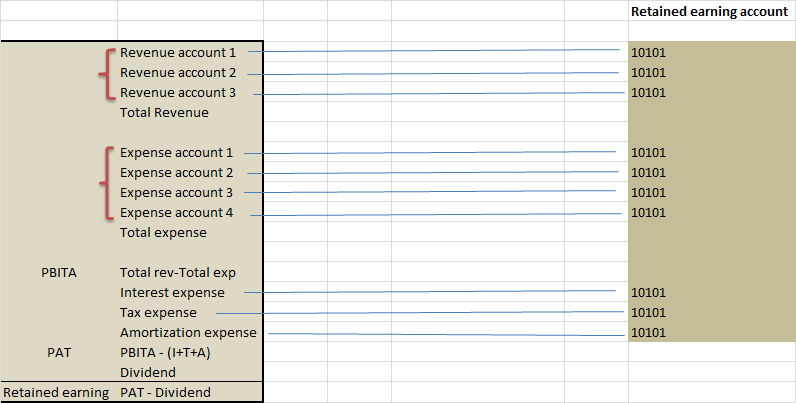

Let’s understand the use of retained earnings account with example:

In below example, GL account 10101 is retained earnings (RE) account which is assigned to every profit & loss account.

At year end, profit & loss balance is carried forward using retained earnings account 10101.

Net amount in 10101 is retained earnings amount. Portion of retained earnings amount can be distributed as dividend or entire retained earnings amount can be capitalized (taken to next year balance sheet under liability).

When company declares dividend below accounting entry is posted:

When dividend is actually paid by the company, below accounting entry is posted

Note: Dividend is a balance sheet item.

GL ACCOUNTING

- What is SAP FICO ?What business requirement is fulfilled in this module?

- What is enterprise structure in sap fico?

- What is GL account? What is account group? What is operational chart of accounts?

- What is the need of country chart of account or alternate chart of account? How country chart of account helps fulfill a business requirement?

- What is the need for group chart of account? How group chart of account helps in consolidation of financial data?

- What is non leading ledger in sap fico?

- What is company code global settings? What global parameter is assigned to company code?

- What is fiscal year variant? Why fiscal year variant is assigned to company code?

- What is posting period variant? Why posting period variant is assigned to company code?

- What is field status variant? What is field status group?

- What is document type in sap? Explain the purpose of document type?

- Document date vs Posting date vs Entry date vs Translation date. Explain

- What is posting key? what is the use of posting key?

- Document header & line items capture information of business transaction.

- Everything about currency & exchange rate in sap.

- Foreign currency valuation in sap. Explain with example

- Retained earnings account helps in year end balance carry forward. Explain

- What is the significance of tolerance groups in sap?

- What parameters are maintained in GL master and how does it impact in document posting?

ACCOUNTS PAYABLE

- What is meant by accounts payable in sap?

- Understanding procure to pay (PTP) cycle and accounting document at each step.

- Understanding MM FI integration in very simple terms.

- Purchase order price determination in SAP. Explained in very simple words.

- House bank, Bank key, Account ID in SAP

- What configuration (FBZP) needed for executing F110 in sap ?

ACCOUNTS RECEIVABLE

- How sap overcomes challenges in accounts receivable process?

- What is customer reconciliation account?

- Understanding order to cash cycle in sap.

- Understanding SD FI integration in very simple terms.

- What is lock box? How lockbox helps in collection from customers?

TAX ACCOUNTING

- How sap helps in tax accounting?

- Tax configuration in sap: Tax procedure, Tax code & Tax jurisdiction code

- Concept of tax jurisdiction code & tax jurisdiction structure

- Significance of “Tax category & Posting without tax allowed” in GL master.

- Tax base amount and Discount base amount

- Assigning tax code V0 & A0 for non taxable transaction?

- Deductible input tax vs non deductible input tax

WITHHOLDING TAX

- Withholding tax in sap explained with example.

- How sap overcomes challenges in managing withholding tax?

- Withholding at the time of invoice or payment

- Withholding tax configuration in sap

- Business place & Section code in sap

- Withholding tax certificate numbering in sap

- Withholding tax report for filling tax returns

ASSET ACCOUNTING

- How sap helps in asset accounting?

- What is meant by asset accounting?

- What is the use of asset class?

- What is the use of depreciation key in asset accounting?

- Depreciation area and Chart of depreciation in sap.

- Derived depreciation area VS real depreciation area?

- Understanding asset accounting configuration needed in sap

- GL account determination for posting asset transaction

- Asset transaction and corresponding accounting document?

- How depreciation is posted in sap?

SAP CONTROLLING