Foreign currency valuation in SAP. Explained with example

In this article we are going to understand foreign currency valuation, foreign currency translation and how exchange rate difference amount is treated while clearing of open item.

Every month end, financial reports need to be prepared for local authority in local currency as well as for group consolidation in group currency.

Foreign currency valuation is about valuating transaction currency amount into local currency amount. Foreign currency translation is about valuating local currency into group currency. Let’s discuss both one by one.

Foreign currency valuation: (Transaction currency to local currency)

Organizations do have transaction in foreign currency. When document is entered in foreign currency (document currency other than company code currency), local currency amount is derived by using currency exchange rate existing at the time of document posting. But later on exchange rate might change hence amount in local currency derived using exchange rate at the time of reporting will not be same as local currency amount in posted document. Impact of exchange rate changes needs to be taken into account by posting adjustment entries.

Example: Company code currency: INR

Group currency: USD

Example 1: On 5th August, I posted vendor invoice of 100 GBP.

(Currency exchange rate type has reference currency USD)

To arrive at exact position of the day of reporting, below adjustment accounting entry should be posted:

This step of posting adjustment entry is referred as foreign currency valuation. Hence foreign currency valuation is needed to incorporate the impact of exchange rate changes.

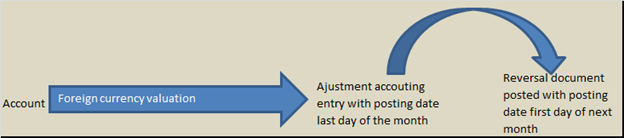

Adjustment accounting entry is posted to get the exact position of balance sheet on the day of reporting. Since this exchange rate gain/loss is unrealized (hypothetical) hence adjustment accounting entry is reversed with posting date in next month.

Standard practice is to run foreign currency valuation on last day of the month which post adjustment accounting entry on last day of the month and reverse the same on first day of next month.

Foreign currency translation: (Local currency to group currency)

Once foreign currency valuation is complete, foreign currency translation is executed to prepare financial report in group currency for consolidation purpose.

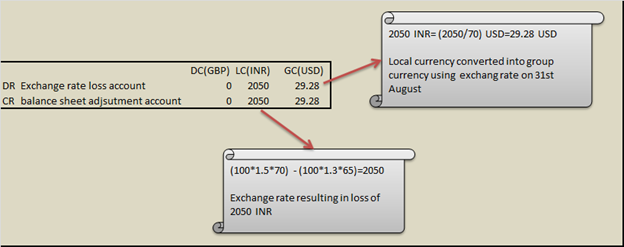

Consider the same above example, foreign currency translation is executed on 31st August

Below document gets posted as a result of foreign currency translation

Adjustment accounting entry is posted to get the exact position of balance sheet on the day of reporting in group currency. Since this exchange rate gain/loss is unrealized (hypothetical) hence adjustment accounting entry is reversed with posting date in next month.

Standard practice is to run foreign currency translation on last day of the month (after foreign currency valuation is complete) which post adjustment accounting entry on last day of the month and reverse the same on first day of next month.

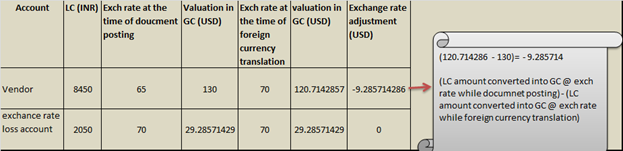

Till now we have been discussing about unrealized gain/ loss which gets originated due to change in currency exchange rates. So the next question, what happens to the realized exchange gain/loss amounts when open item is cleared?

How sap treats realized exchange rate difference amount?

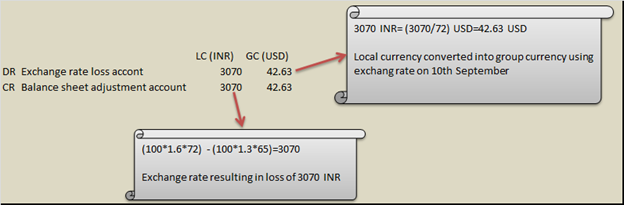

Example: Let’s say vendor payment is being done on 10th September.

(Currency exchange rate type has reference currency USD)

Payment amount is 100 GBP.

Invoice will get cleared with payment document and an adjustment accounting entry will get posted as below

In this example, impact of exchange rate change is realized (vendor open item has been cleared) hence no need to post reversal of adjustment accounting entry. Reversal entry is posted for unrealized exchange gain or loss.

What are the accounts relevant for foreign currency valuation?

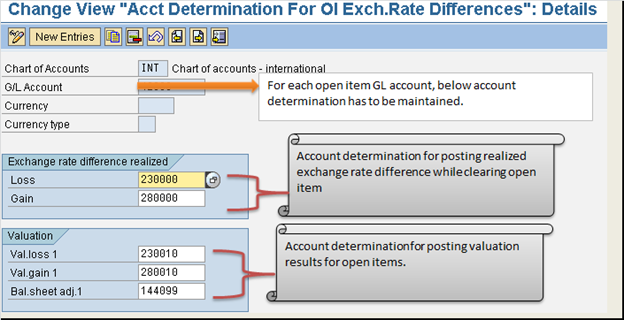

Accounts which are managed on open item basis and have foreign currency transaction. E.g. clearing accounts, GR/IR clearing account, reconciliation account etc.

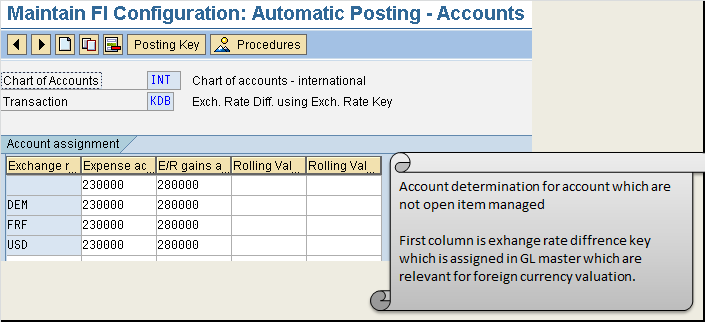

Accounts which are not managed as open item and have foreign currency transaction e.g. Bank accounts, sales account etc.

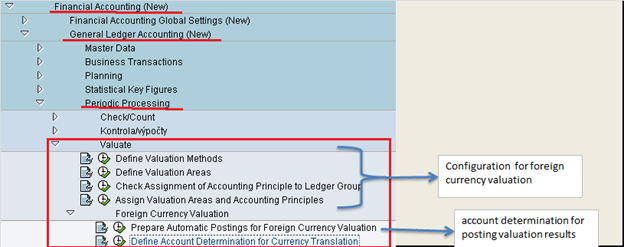

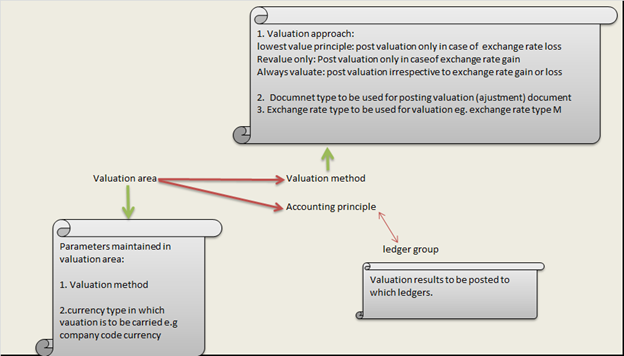

What configuration is needed for foreign currency valuation and translation?

Below shows place where account determination is maintained for accounts which are managed on open item basis:

Account determination for GL accounts which are not managed on open item basis but are relevant for foreign currency valuation.